Kisan Vikas Patra (KVP) is a small savings instrument launched by the Indian Government to encourage long-term savings. Originally aimed at farmers to promote small savings in rural areas, KVP has grown popular among people looking for a safe investment avenue with predictable returns.

What is Kisan Vikas Patra?

Kisan Vikas Patra is a fixed-rate savings scheme available at India Post Offices and select public sector banks. The scheme offers assured returns on investment and provides capital appreciation by doubling the investment over a fixed tenure. KVP is popular due to its government backing, providing a low-risk investment option that appeals to conservative investors.

Key Features of Kisan Vikas Patra

| Feature | Details |

| Minimum Investment | ₹1,000 (in multiples of ₹100) |

| Tenure | Around 115 months (9 years and 7 months) |

| Interest Rate | 7.5% per annum (varies per quarter) |

| Tax implications | No tax benefit on initial investment; interest is taxable |

| Premature Withdrawal | After 2.5 years, with reduced returns |

| Guarantee | Backed by the Government of India |

| Nomination Facility | Available |

Note: The interest rate on KVP is subject to periodic changes by the government, typically announced every quarter.

How Does Kisan Vikas Patra Work?

When you invest in KVP, your money is guaranteed to double in 115 months at the current interest rate of approximately 7.5%. The scheme uses a compound interest formula, meaning your investment grows steadily over the term. KVP certificates are available in denominations from ₹1,000 upwards, and there is no upper investment limit.

Eligibility Criteria for KVP

· Individuals: Indian citizens above 18 years of age can invest.

· Minors: Investments on behalf of minors are allowed.

· NRIs: Non-Resident Indians are not eligible for KVP.

Benefits of Kisan Vikas Patra

1. Government Security: Since KVP is a government-backed scheme, it provides high security for investors.

2. Guaranteed Returns: Investors receive a guaranteed return, with the assurance that the investment will double in the prescribed period.

3. Ease of Access: KVP certificates are available at all post offices and select banks, making it easy to purchase.

4. Transferable Certificates: KVP certificates can be transferred from one person to another or from one post office/bank to another, offering flexibility.

5. No Investment Cap: There is no maximum limit on investment, making KVP suitable for those with high investable surplus seeking low-risk returns.

Comparing Kisan Vikas Patra with Other Small Savings Schemes

| Scheme | Interest Rate (approx.) | Lock-in Period | Tax Benefit (Sec 80C) | Premature Withdrawal |

| Kisan Vikas Patra | 7.5% p.a. | 9 years, 7 months | None | After 2.5 years |

| Public Provident Fund (PPF) | 7.1% p.a. | 15 years | Yes | Partial after 5 years |

| National Savings Certificate (NSC) | 7.7% p.a. | 5 years | Yes | Not allowed |

| Senior Citizens’ Savings Scheme (SCSS) | 8.2% p.a. | 5 years | Yes | Penalty after 1 year |

| Fixed Deposit (Bank) | Varies (5-7% approx.) | Flexible | Yes | Penalty on early withdrawal |

KVP Tax Implications

1. No Tax Deduction under Section 80C: Unlike PPF or NSC, investments in KVP do not qualify for tax deductions under Section 80C.

2. Tax on Interest Income: The interest earned is added to the investor’s taxable income each year and is subject to tax as per applicable income tax slabs.

3. No TDS on KVP Interest: No Tax Deducted at Source (TDS) is applied on the amount withdrawn post maturity. However, this does not exempt you from declaring the interest income in your income tax returns (ITR) and paying tax accordingly.

Who Should Invest in Kisan Vikas Patra?

KVP is ideal for conservative investors who prioritize safety and guaranteed returns over high growth. It is particularly suited for:

1. Individuals with Low-Risk Appetite: KVP provides guaranteed returns without exposure to market volatility.

2. Investors Seeking Long-Term, Safe Investments: The scheme is beneficial for those who want to grow their money steadily without taking risks.

3. Senior Citizens and Rural Investors: These groups typically prefer secure investments with government backing.

How to Invest in Kisan Vikas Patra?

1. Visit a Post Office or Authorized Bank: Go to a nearby post office or authorized bank branch that offers KVP.

2. Complete KYC Process: Submit proof of identity, address, and other KYC documents.

3. Fill Out the Application Form: Fill in the required details, including nominee details.

4. Payment: Make the payment in cash, cheque, or demand draft.

5. Receive KVP Certificate: Upon verification, the KVP certificate is issued in the investor’s name.

Historical Interest Rates for Kisan Vikas Patra

| YEAR | RATE OF INTEREST (%) |

| 23-09-2014 to 31-03-2016 | 8.7(100 Months) |

| 1.4.2016 to 30.9.2016 | 7.8 (110 Months) |

| 1.10.2016 to 31.3.2017 | 7.7 (112 Months) |

| 1.4.2017 to 30.6.2017 | 7.6 (113 Months) |

| 1.7.2017 to 31.12.2017 | 7.5 (115 Months) |

| 1.1.2018 to 30.9.2018 | 7.3 (118 Months) |

| 1.10.2018 to 30.6.2019 | 7.7 (112 Months) |

| 1.07.2019 to 31.03.2020 | 7.6 (113 Months) |

| 1.4.2020 to 30.09.2022 | 6.9(124 Months) |

| 1.10.2022 to 31.12.2022 | 7.0(123 Months) |

| 1.01.2023 to 31.03.2023 | 7.2(120 Months) |

| 1.04.2023 to 31.12.2024 | 7.5(115 Months) |

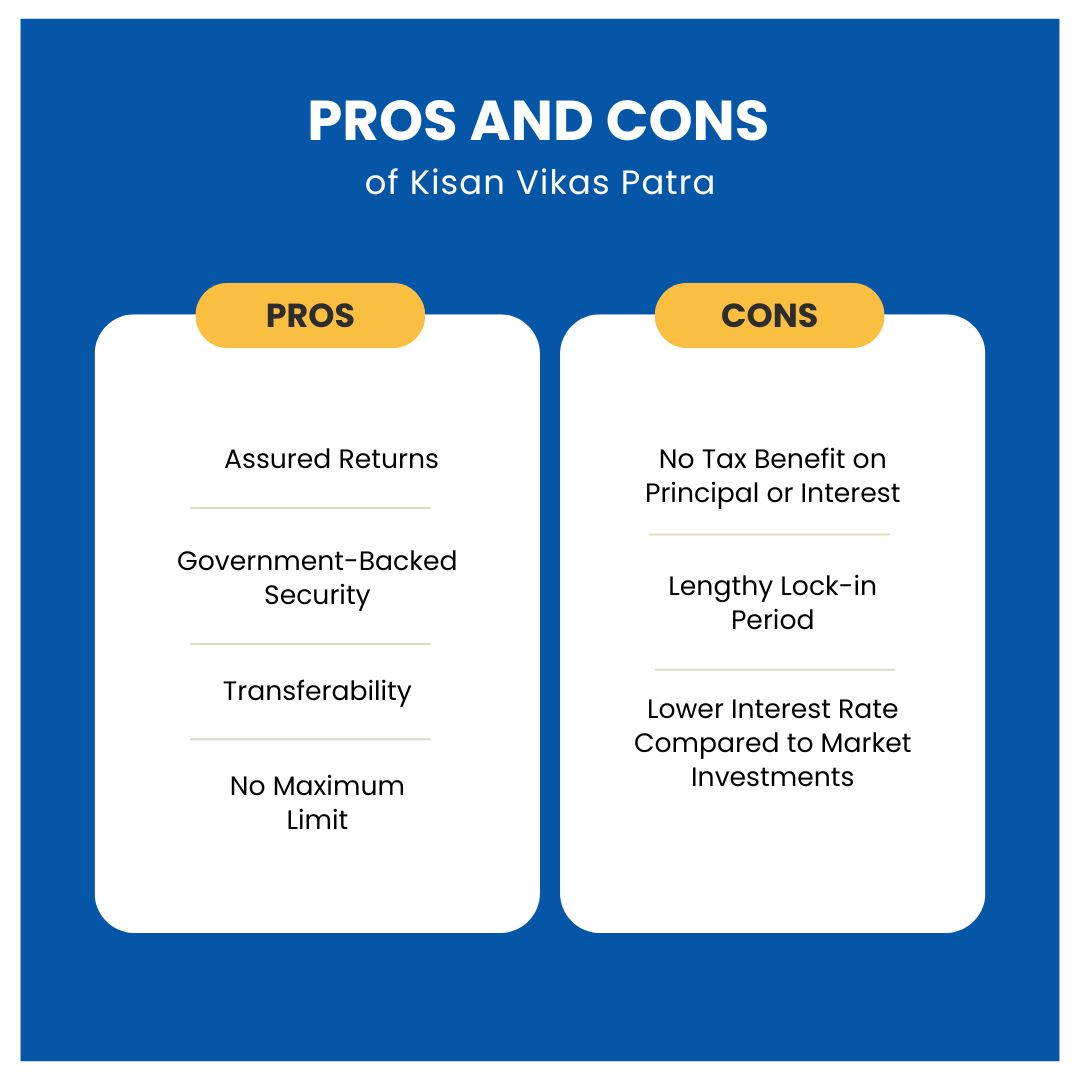

Pros and Cons of Kisan Vikas Patra

Pros

· Assured Returns: Guaranteed return on investment.

· Government-Backed Security: Low risk due to government support.

· Transferability: Can transfer ownership, making it flexible.

· No Maximum Limit: No upper limit on the amount invested.

Cons

· No Tax Benefit on Principal or Interest: Interest earned is taxable.

· Lengthy Lock-in Period: Maturity period of 10 years and 4 months can limit liquidity.

· Lower Interest Rate Compared to Market Investments: The rate of return is lower than some market-linked products like mutual funds.

Conclusion

Kisan Vikas Patra is a solid investment choice for risk-averse individuals who value security and assured returns. While the returns may not be as high as market-linked investments, the guarantee of doubling the investment makes it a reliable option, particularly in times of economic uncertainty. However, potential investors should weigh the lack of tax benefits and consider their liquidity needs before committing to KVP.